")

Overstock: Buy For E-Commerce Leadership, Stay For Crypto Potential (NASDAQ:OSTK)

Table of Contents

ipopba/iStock via Getty Images

Overstock.com, Inc. (OSTK) delivered one of the most impressive financial turnaround stories you’ll find on Wall Street. Going back to 2019, the home goods e-commerce pioneer was struggling to remain relevant with mounting losses and a criticized strategy pivot towards blockchain tech. Fast forward, the stars aligned during the pandemic driving a boost to its online retail business while the company also benefited from momentum in the crypto space.

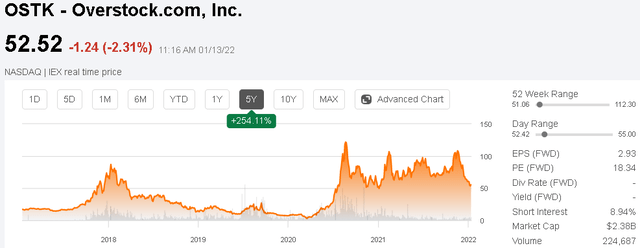

Indeed, from a low of $2.53 per share in Q1 2020, OSTK ultimately climbed to $128 per share with the story backed by real earnings. Fast forward, the stock has since corrected lower amid broader market volatility, but the key point here is that the outlook remains positive. We are bullish on OSTK which offers a unique combination of solid fundamentals in a core free cash flow generating business with significant long-term growth opportunities in blockchain technologies.

Seeking Alpha

OSTK Financials Recap

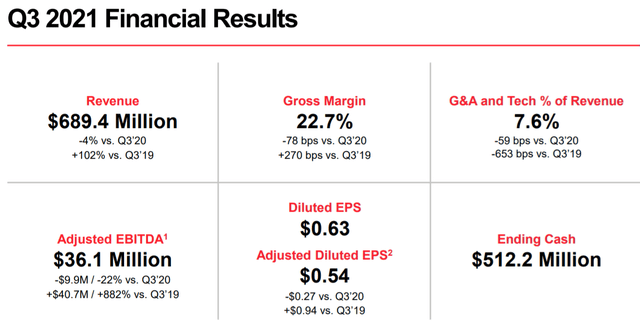

The company last reported its Q3 results in late October with EPS of $0.63, which was $0.23 above expectations. Revenue of $689 million, fell by 4% y/y but was also ahead of market estimates. The context here is the comparison period in Q3 2020 that was defined by the early stages of the economic recovery with themes like stay-at-home and demand for home goods amid a hot housing market leading to an exceptional quarter.

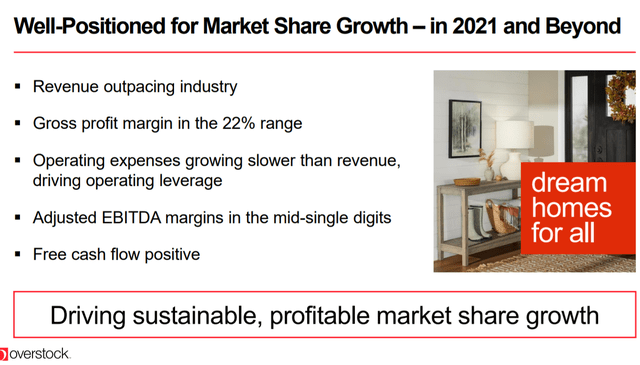

In this regard, the results this year have been defined by overall resiliency, with sales still up 102% compared to Q3 2019 as a pre-pandemic benchmark. Similarly, the gross margin in the quarter at 22.7%, while down 78 basis points from the period last year, is up from 20.0% on a two-year stacked basis.

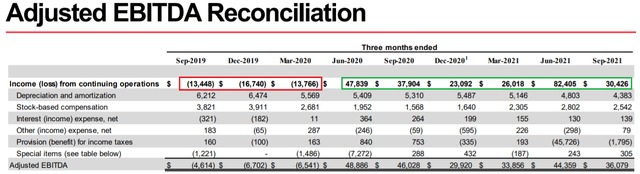

Overstock has been able to translate its higher top-line sales into what is now more consistent profitability through scale. G&A expenses have declined significantly as a percentage of revenue to 7.6%, from as high as 15.8% in early 2020. The result is that adjusted EBITDA this last quarter at $36.1 million reverses a loss of -$13.4 million in Q3 2019 as one of the best indicators describing the financial turnaround we have mentioned. Through the first nine months of the year, Overstock has generated $90 million in free cash flow. This was the 6th consecutive quarter of positive earnings.

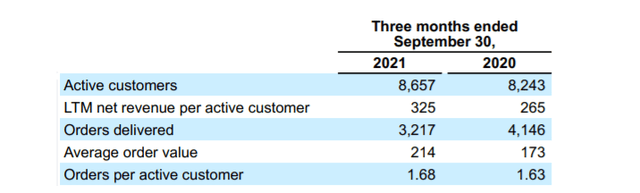

Management has noted an effort to refocus its merchandise selection in home goods and furnishings while removing unrelated categories. This is expected to streamline the operations and support margins going forward. The company ended the quarter with 8.7 million active customers, up from 8.2 million in Q3 2020. While the number of orders delivered declined 22% y/y considering the difficult comps, the trend has been a material increase in the average order value that has reached $214 from $173 last year with customers effectively spending more on the site.

Finally, we note that Overstock ended the quarter with $512 million in cash and equivalents against just $39 million in long-term debt. We view the balance sheet and liquidity position as a strong point in the company’s investment outlook.

In terms of guidance, management expects to continue growing market share within home goods and furnishings. General targets for the year include a gross margin in the 22% range, in line with the Q3 result. The company expects to deliver EBITDA margins in the mid-single digits as well as continued positive free cash flow.

OSTK as a Crypto Play

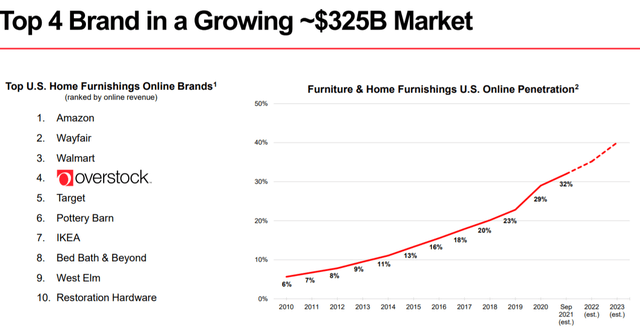

From a high level, one of the major tailwinds for the segment is data showing that the online penetration of furniture & home furnishings has climbed from around 18% in 2017 to a current level estimated around 32%, gaining share from brick-and-mortar channels. Overstock is the number four brand next to other e-commerce giants like Amazon.com, Inc. (AMZN), Wayfair Inc. (W) and Walmart Inc. (WMT) as the largest players in the category by online revenue. Beyond the current post-pandemic volatility and near-term headwinds related to consumer inflationary pressures, we see Overstock well-positioned to grow and consolidate its market share given its positioning with a focus on “smart value” merchandising.

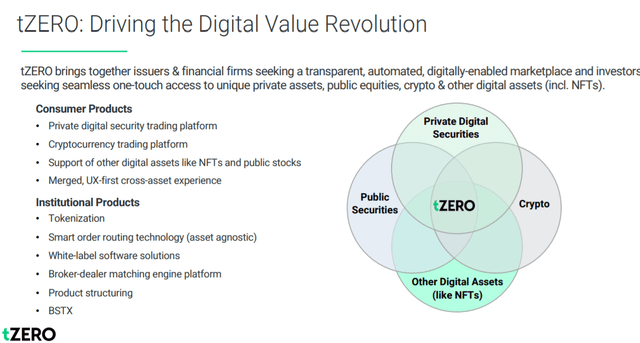

That said, what makes OSTK particularly interesting are its investments in blockchain technology and the broader crypto space through its “Medici Ventures” segment. Consolidated within the overall financial results, the company has been active in the segment over the past several years building a portfolio of start-ups focusing on applications across including capital markets, identity, supply chain, and financial services.

tZero is the highlight of the group representing a trading platform for digital assets with a differentiation focusing on institutional grade solutions for private companies looking to digitize their capital and trade on a regulated market. The tZero app as a consumer product allows trading between private securities and tokens, along with regular cryptocurrencies like Bitcoin (BTC-USD), as well as other digital assets including non-fungible tokens (NFTs).

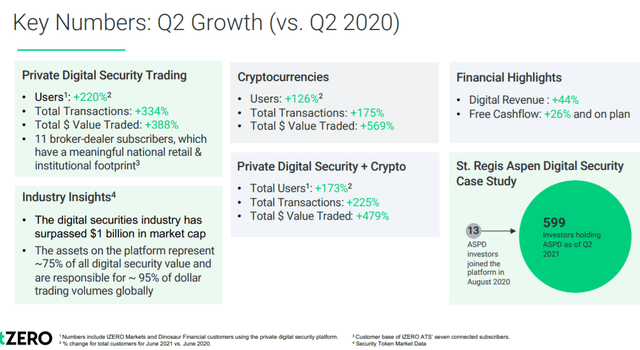

The last update from Q2 data by tZero showed significant operating momentum with users on the platform up 173% y/y between private digital securities and crypto trading. The value of all transactions traded has climbed 479% compared to the period in 2020. In October it was announced that tZero received authorization from FINRA, a financial market regulator, to self-clear and settle trades as a registered broker-dealer. The move is expected to provide new growth opportunities.

While the financial contribution from Medici and tZero is still small relative to the broader Overstock e-commerce business, we believe it gives the company an incremental bullish case. It’s clear that shares of OSTK have benefited from the momentum surrounding “cryptocurrencies” since the asset class broke out in 2020. On this point, we last published a bullish article on OSTK back in April of 2020 and it’s fair to say the evolution of the company has surpassed our expectations.

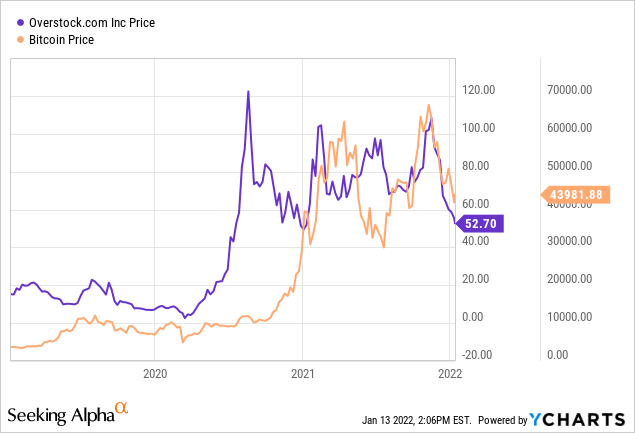

Looking ahead, it’s clear that OSTK will maintain some correlation to the crypto space with the trading action in Bitcoin as a benchmark for the sector sentiment. Notably, shares of OSTK have sold off from a high of $110 which coincided with the cycle high in Bitcoin that reached $69k right around the same time. We believe OSTK can rally alongside cryptocurrencies to the upside as it implies a higher valuation for Medici Ventures and tZero as a backdrop for a positive operating outlook and more growth opportunities.

OSTK Stock Forecast

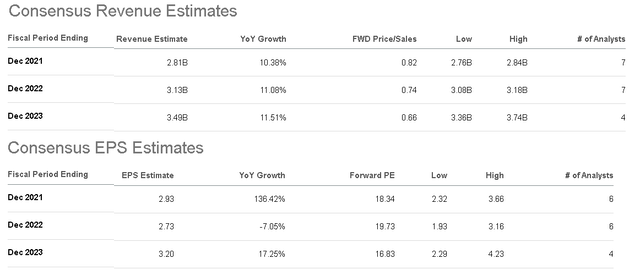

While a date has not yet been confirmed, Overstock will likely report Q4 results in mid-February. According to consensus estimates, the forecast is for full-year revenue to reach $2.8 billion, up 10% compared to 2020. An EPS estimate of $2.93, if confirmed, will represent an increase of 136% year over year. Looking ahead, the market sees the top-line momentum averaging around 10% over the next two years, while there is room for EPS to trend towards $3.20 by 2023.

Seeking Alpha

Again, these estimates are largely based on the core retail business. It’s a tricky environment considering the company faces a more difficult comparison period into 2022 against the start of 2021. Last year the stimulus payments to consumers likely boosted sales at the time. Current themes like elevated inflation and Omicron Covid disruptions add a layer of macro uncertainty. The recent weakness in the crypto segment also has the potential to drag sentiment towards OSTK lower.

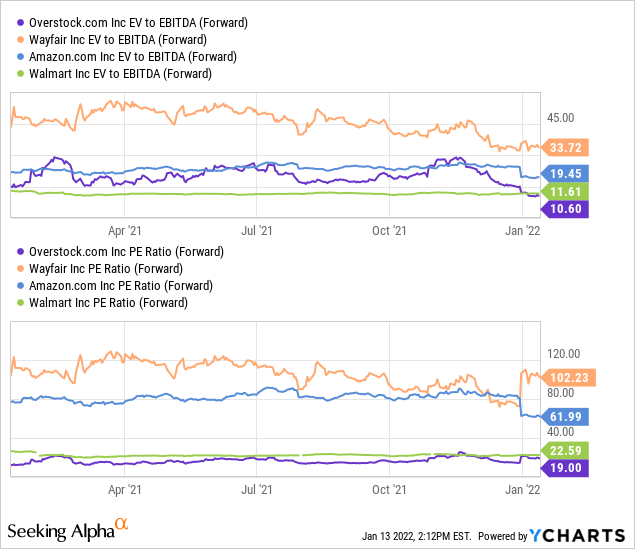

Nevertheless, we highlight what is a compelling valuation for the stock considering an EV to consensus EBITDA at just 11x and a forward P/E ratio of 19x. This is in contrast to Wayfair as the most direct comparison with an online home furnishings leader. In this case, Wayfair also benefited from a boost in sales during the pandemic trades at a forward P/E of 102x and EV to forward EBITDA of 34x. Valuation multiples for OSTK are also at a discount compared to Amazon and Walmart as a reference point among mega-cap leaders of e-commerce.

While it’s fair to say some of these companies deserve a premium given their larger scale and global diversification, we make the case that OSTK is cheap considering its high growth in blockchain and crypto sector tech investments. The numbers are even more attractive considering Overstock has over $470 million in net cash on its balance sheet.

OSTK with a current market value of $2.2 billion and the tZero investment with a carrying value of $329 million on the balance sheet, we make the case that investors are buying the e-commerce business and effectively getting the entire Medici fund as an incremental bonus. The optionality embedded in this setup makes OSTK a unique reward to risk opportunity.

Final Thoughts

Recognizing the near-term uncertainties and some macro headwinds, we are bullish on OSTK viewing the recent correction as a buying opportunity. The stock down more than 50% from its recent highs has likely helped balance valuation concerns while likely already pricing in some of the worst operating scenarios.

We rate OSTK as a buy with a price target for the year ahead at $70 per share representing a forward P/E of 25x. At this level, we believe OSTK would be more fairly valued given its financial strength and positive operating outlook relative to home goods e-commerce peers. To the upside, the potential that the crypto sector regains momentum or that the tZero platform gains market traction can lift shares higher.

Risks to consider include the company’s exposure to high-level consumer spending trends and the possibility of a broader economic slowdown. Weaker than expected results over the upcoming quarter would force a reassessment of the company’s earnings outlook. In the current market environment, expect volatility to continue which keeps OSTK in the high risk and speculative category.