5 Stocks For A New Bull Industry

Table of Contents

Bet_Noire

By Brian Nelson, CFA

Artificial intelligence is here. Inflation appears tamed. Unemployment is continue to close to all-time lows. The household housing market place is keeping up. The stock industry stays resilient supporting family wealth. The Fed has elevated prices substantially, translating into large potential dry powder to encourage equities. The banking system was challenged nevertheless yet again with SVB Monetary (OTCPK:SIVBQ) and confirmed that governing administration businesses ended up completely ready to act and in a major way to preserve the economical technique seem. The regular goings-on and tit-for-tat with China, North Korea and Russia carry on, but which is practically nothing out of the ordinary. Asset allocators once again have been burnt by shifting into bonds as major cap tech and huge cap development rallied considerably so considerably in 2023.

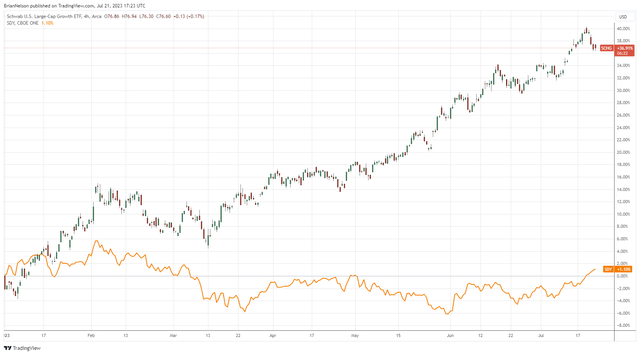

The area of substantial cap progress is up about 40% so considerably in 2023 though dividend development investing is approximately flat. (TradingView)

What does all this indicate? Well, we imagine it really is a new bull market in equities, and in this write-up, we emphasize 5 stocks to take into account for the good occasions to appear. Lots of of the shares underneath pay out a dividend, but it is really significant to take note that a aim on dividends should not be the principal location of concern for buyers. For case in point, as we notice in this posting, superior produce investing and dividend growth investing could have expense retirees tremendously all through the previous ten years or so. When it comes to the dividend, it’s significant to assume of it this way: If you have a $10 inventory, and it pays a dividend, you now have a inventory that is $9 and a $1 in dividends. That is how it functions. With that claimed, let’s dig into 5 of our beloved thoughts for this new bull market place!

Microsoft Corp. (MSFT)

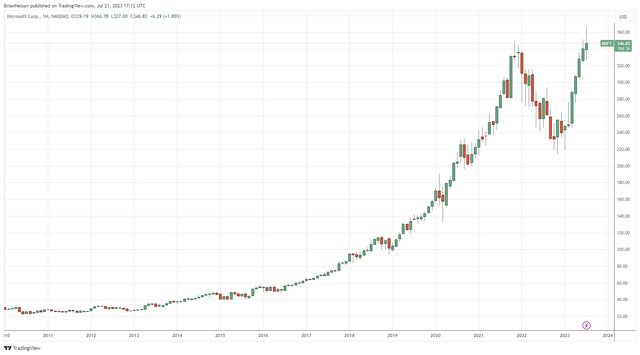

Microsoft’s shares have had a wonderful run. (TradingView)

Microsoft, by much, is a person of the finest techniques to engage in the proliferation of artificial intelligence. The enterprise has already rolled out AI throughout some of its products for a pleasant action-transform in price tag, and we would anticipate price boosts to continue on as additional and extra users see incredible worth in its AI resources. The firm is doing the job to near its proposed acquisition of Activision Blizzard (ATVI), and when we generally do not like the all-cash deal, we are beginning to feel that upside over the upcoming 10 years for this transaction might switch out to be drastically material as Microsoft put up-offer carries on to re-develop a war upper body of web money on the books as its gaming belongings proliferate. We ended up pretty cautious on its prior acquisition of LinkedIn, and we were probably erroneous about becoming skeptical on the offer when it turned out to be a good just one. We are probably completely wrong about being careful on Activision, also, as it could pave the way for major synergies throughout the firm’s solution suite. We’re huge followers of Microsoft and feel the corporation will continue to be a primary driver guiding the strength in big cap tech and massive cap expansion.

Apple Inc. (AAPL)

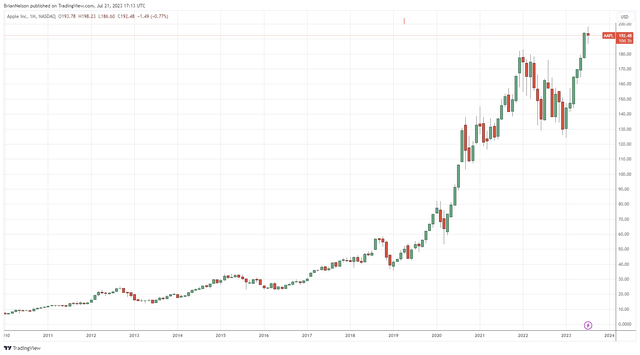

Apple’s shares just lately broke out, and we go on to like its strengthening fundamentals. (TradingView)

Apple is just phenomenal and meets a great deal of the standards we glance for in a excellent investment decision notion thought. But very seriously, what can we say about Apple that hasn’t now been reported? Perfectly, truth be instructed, we’re not versus repeating what Warren Buffett not too long ago reported about the organization:

“The superior factor about Apple is (Berkshire) can go up (in our ownership stake). They maintain obtaining their stock alternatively of our proudly owning 5.6%, if they get down to… 15.25 billion of shares exceptional, without our accomplishing something we got 6%. Our requirements for Apple is not unique than the other organizations we personal it just comes about to be a superior business enterprise than any we individual. And we place a fair volume of funds in it… and our railroad small business is a extremely superior enterprise, but it is not remotely as fantastic as Apple’s company. Apple has a place with people where by they are spending $1,500 or whichever it may perhaps be for a cellular phone, and these very same people fork out $35,000 for getting a next motor vehicle, and if they had to give up their second vehicle or give up their Apple iphone, they’d give up their 2nd motor vehicle. I indicate it can be an remarkable (item). We never have just about anything like that that we individual 100% of… but we are extremely, extremely, extremely, pleased to have 5.6% or whatever it might be p.c (of Apple), and we’re delighted each individual tenth of a percent that it goes up.”

Apple’s items are an really useful element of client lifetime, and we love the firm’s huge net hard cash situation and major totally free income circulation — two of the most important income-centered sources of intrinsic worth. We expect the firm’s Apple iphone to continue to be a enthusiast-most loved, and its Products and services business enterprise and entrenched mounted foundation are ripe for upselling and cross-advertising chances, whether it be in AI or other locations. We’re enthusiastic about the firm’s ‘Vision Pro’ and anticipate some significant figures in fiscal 2024. We will not feel Apple will disappoint.

UnitedHealth Group (UNH)

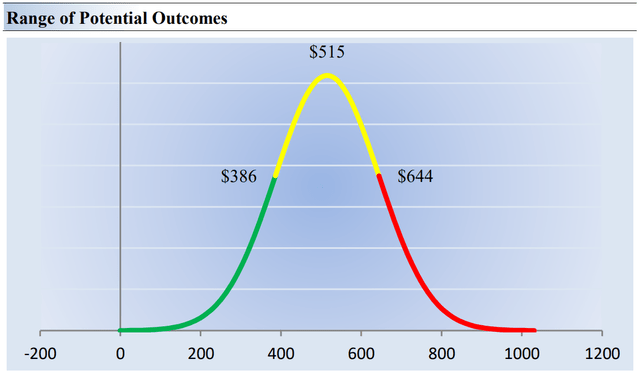

Our good value estimate variety for UnitedHealth Team. (Valuentum)

Big cap tech tends to dominate the headlines these times, but there is a substantial cap development entity that is held in the exact esteem by us. That organization is UnitedHealth Group. Shares of UnitedHealth Group just lately came underneath force with considerations in excess of enhanced health care fees as discretionary surgical procedures select up subsequent a slowdown all through the COVID-19 pandemic, but we think UnitedHealth Team will finally be equipped to re-value proficiently to get well the improved prices.

UnitedHealth Team is a rare huge cap growth strategy that is trading at the decreased stop of our reasonable price estimate vary ($386-$644 for each share). In some methods, UnitedHealth Team can be viewed as an undervalued, progress-oriented equity with a great dividend yield. These attributes could bring in a large amount of shopping for, as the inventory is appealing to a terrific quantity of investors. Our level truthful value estimate for UNH stands at $515 for every share, and the business boasts a ~1.5% ahead estimated dividend yield.

Visa Inc. (V)

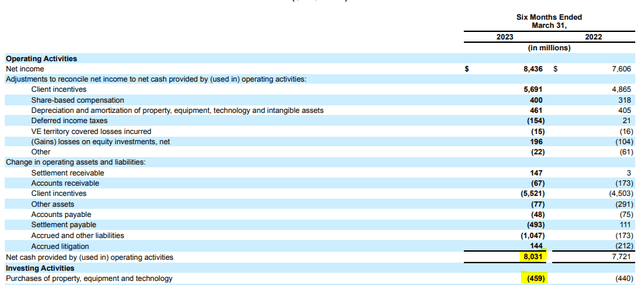

Visa’s working income movement of $8 billion, and totally free hard cash stream of ~$7.5 billion through the initial half of its fiscal 2023 is exceptional. (Visa)

Visa most likely has the very best company model out there. The credit history card huge benefits from a network result, functions as a toll-street operator as it collects a fee just about every time a single of its playing cards is swiped. It also places up significant operating and no cost cash movement margins. The organization is a leading consideration in the portfolio of our Best Tips Publication, and we do not see that switching at any time soon.

Visa’s speed of expansion continues to flip heads, too, and its free of charge money circulation generation stays amazing. Working funds movement has arrive in at ~$8 billion through the to start with six months of the calendar year, when the business shelled out ~$460 million in funds spending, fantastic for cost-free hard cash move technology of ~$7.5 billion and a free dollars move margin of 47.5%. Pretty several other providers have this kind of totally free money stream margin, and we glance ahead to a solid back 50 percent to Visa’s fiscal 2023. Visa is definitely a single for thought throughout this new bull market.

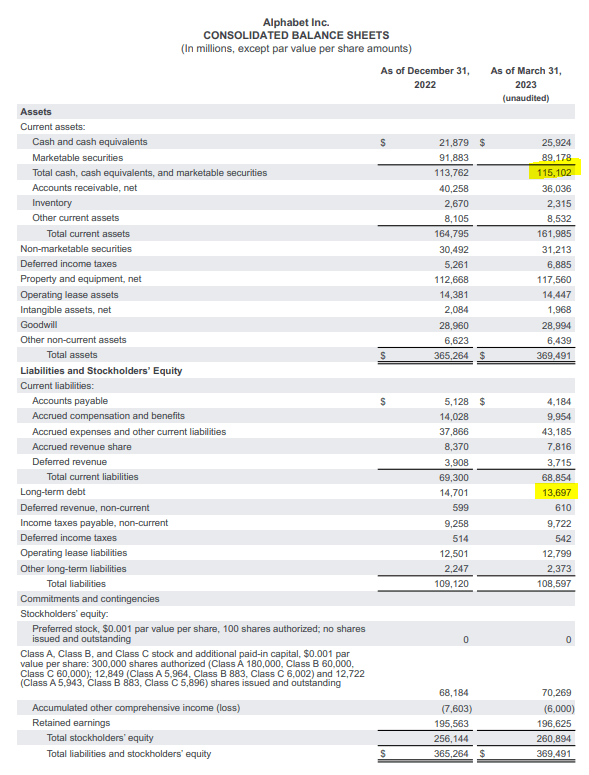

Alphabet’s equilibrium sheet is excellent! (Alphabet)

In a person of our latest notes, we famous the pursuing:

“Alphabet stays a single of our preferred providers… many thanks to its tremendous internet-money-loaded harmony sheet and future anticipations of free hard cash movement… Alphabet has upside in AI, and the world wide research market is massive and rising rapid enough that we don’t anticipate level of competition to consume Alphabet’s lunch. But even if Alphabet does sooner or later shed share in lookup, it would most likely be Microsoft’s Bing that would take it, and that’s basically a very good point for substantial cap growth (provided Microsoft’s weighting in this spot, far too). Even if Alphabet falters, large cap development might not.”

We wanted to contain an picture of Alphabet’s most new equilibrium sheet as nicely. When we say that a firm has a great net income placement, we signify that its cash on the balance sheet is drastically greater than its personal debt place.

As revealed in the image higher than, Alphabet has ~$115.1 billion in total funds, funds equivalents, and marketable securities, although it has just ~$13.7 billion in very long-time period financial debt, very good for a web dollars situation of $101.4 billion in internet dollars, which is higher than lots of of the market place capitalizations of corporations in the S&P 500.

We enjoy this characteristic of Alphabet as it provides the firm great monetary overall flexibility, and if the organization have been to at any time place this war chest of excess money to function, it would likely be a constructive catalyst, in our see. If Alphabet ended up to get even extra intense with buybacks or scoop up undervalued assets, we’d anticipate the inventory to pop noticeably.

Concluding Views

We’re loving what we consider is a new bull current market, and it would seem like all the pieces of the puzzle have fallen in location for a further fantastic 10 years of equity returns. We think the leaders of this new bull market place will continue on to be in the parts of massive cap tech and huge cap growth, and this short article highlights 5 of our favorites for thought. Investors may perhaps be clever to steer crystal clear of substantial produce equities these as these identified in property finance loan REITs, master limited partnerships, REITs and instead contemplate the internet-hard cash-abundant and strong free income flow turbines within the locations of big cap tech and massive cap progress. Enable the great periods roll!

This write-up and any one-way links within just are for informational and educational reasons only and really should not be viewed as a solicitation to acquire or offer any safety. Valuentum is not dependable for any glitches or omissions or for final results attained from the use of this posting and accepts no legal responsibility for how readers may possibly select to make the most of the content. Assumptions, thoughts, and estimates are based mostly on our judgment as of the date of the write-up and are topic to adjust without recognize.